The distinction between tokenised and traditional funds is disappearing

- 7 hours ago

- 5 min read

Contrary to popular opinion, institutional investors in tokenised funds value intermediaries for providing assurance and seamless links with traditional assets

Tokenised funds are not only reaching new classes of investors but future-proofing asset managers against the coming generation of digital native investors

Trading practices, and regulatory reforms, are eroding the distinctions between tokenised funds and traditional funds, securities and money markets

The growing interest of institutional investors in cryptocurrencies is allied to rising demand for yield on cryptocurrency investments. This necessitates active management, which creates challenges. Neither Exchange Traded Funds (ETFs) nor conventional mutual funds issued under the Investment Company Act of 1940 (’40 Act funds) can accommodate actively traded cryptocurrency funds.

Which is why, when Coinbase Asset Management launched the Coinbase Bitcoin Yield Fund (CBYF) for institutional investors in April 2025, it chose a private, Cayman-domiciled master-feeder hedge fund. However, this created further challenges. An actively managed Bitcoin fund needs access to multiple cryptocurrency exchanges, the ability to source and deploy collateral and openness to any custodian an investor chooses.

In March 2026 Coinbase Asset Management introduced a further complication by adding a tokenised share class to the CBYF. The purpose was to increase the appeal of the fund to family offices, high net worth investors (HNWIs) and corporate treasurers that are comfortable trading and financing funds entirely on-chain, including the use of Stablecoins instead of traditional banks to provide a settlement asset and cash collateral.

Counter-intuitively, these digitally native investors do not prefer digitally native funds. In fact, they are wary of digitally native funds, preferring the assurance of access to an underlying asset at a custodian and a transfer agent to maintain a register of ownership. It also means they do not have to use separate issuance, trading and servicing infrastructures to invest in tokenised and traditional funds.

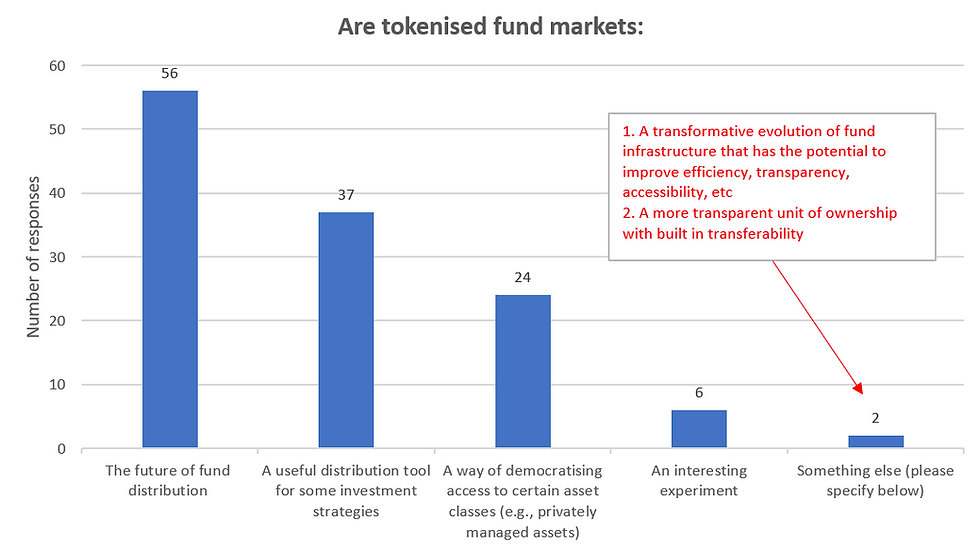

Chart 1

This helps to explain why half the webinar audience believe that the benefits of fund tokenisation are not dependent on fully native tokenised funds (see Chart 1). True, a third of the audience did think that the benefits of tokenisation depend on fully native funds – and chiefly because native funds can dispense with intermediaries such as custodian banks, paying agents and transfer agents.

However, recent regulatory changes in the Cayman Islands have also favoured retention of transfer agents to record issuances, transfers and ownership. Ironically, the amendments to the Mutual Funds Act, Private Funds Act and the Virtual Asset (Service Providers) Act (VASP Act), enforced by the Cayman Islands Monetary Authority (CIMA) from 24 March 2026, were made to accommodate tokenised funds.

In short, retention of transfer agency is not a victory for traditionalism but a consequence of choosing to regulate tokenised funds domiciled in the Cayman Islands in the same way as traditional funds domiciled in the Cayman Islands. The alternative was regulation under the VASP Act, or some combination of several pieces of legislation, fostering a degree of legal uncertainty that is scarcely conducive to issuance activity.

As the link between subscriptions and redemptions – or secondary market sales and purchases - transfer agents are crucial to the successful distribution of funds. One role they play is ensuring that digital assets are not mis-sold, either to investors for whom the asset is not appropriate, or to criminals such as money launderers, terrorists and sanctions evaders.

Indeed, one reason why a substantial minority of the webinar audience (see Chart 2) believe tokenisation can enhance distribution is that investor eligibility can be built into tokenised funds using smart contracts. These embed the distribution restrictions of a fund prospectus into the tokens themselves: they cannot be transferred to a digital wallet that is not white-listed, pre-qualified and validated by the transfer agent.

Chart 2

Another reason that the audience believes tokenisation aids distribution is that tokenised funds can reach wider classes of investor. This is obvious in the case of on-chain investors operating digital wallets. They appreciate the ability to use tokenised assets of all kinds as collateral to raise finance. It is why tokenised money market funds have proved so popular with these investors.

But tokenisation also makes it possible to distribute funds to investors that would not normally be able to afford the minimum subscription amount. Tokens are available in smaller (or fractionalised) amounts. Indeed, this can be seen as the principal purpose of fund tokenisation: to reach investors that are not accessible through traditional fund distribution networks.

They may never be accessible by traditional means. There is a view that the younger, digitally native investors that are about to come into their inheritance from their ageing Boomer parents will never buy a conventional fund via a conventional distributor using cash stored at a conventional bank. The tokenisation of funds opens the digital channels that reach these investors.

However tokenised funds are distributed, and whoever they are distributed to, it nevertheless falls to transfer agents to keep the records of tokenised and traditional fund transactions and ownership records synchronised. However, individual transfer agents cannot solve the industry-wide lack of interoperability between blockchain protocols, private and public blockchains and blockchains and traditional networks.

This lack of interoperability is often cited as a major barrier to the scaling of tokenised asset markets. But to some extent centralised exchanges are addressing it already by obliterating silos. Users of Coinbase, for example, can already trade on a single platform cryptocurrencies, cryptocurrency derivatives, tokenised funds and traditional listed exchange-traded funds (ETFs) and equities, using a single digital wallet.

It is also questionable whether traditional securities markets deliver interoperability. In effect, one asset can be exchanged for another only by selling and buying for cash. Stablecoins mean the going-to-cash model of exchange is being reproduced on blockchains, even though in principle tokenisation means one digital asset can be exchanged for another without reverting to cash.

On-chain swaps are not happening because there is insufficient liquidity - in the sense of how quickly an asset can be turned into cash - in tokenised assets on-chain. But if the immediate barrier to scale is not interoperability but illiquidity, tokenisation can clear the barrier only if it becomes possible to move tokenised assets issued on to different blockchains between digital wallets anywhere.

Ultimately, illiquidity and interoperability are different expressions of a single problem. Centralised exchanges – of the cryptocurrency as well as the traditional kind - cannot solve it because they remain closed universes, as do proprietary blockchain protocols. Only a global marketplace in tokens that trades 24/7/365 can generate the liquidity to achieve scale, and that depends on making all pools of liquidity interoperable.

Interestingly, the audience argue that traditional intermediaries protecting their existing rents are not the principal barrier to reaching that Nirvana. A mere quarter contend that the benefits of fund tokenisation hinge on disintermediating transfer agents, fund accountants and custodians (see Chart 3). Two thirds are more excited about wider distribution and technical benefits such as fractionalisation and composability.

Chart 3

This does not mean, of course, that incumbents reliant on legacy technology will not disappear. But it implies they will disappear because they failed to rise to the opportunity, not because they were unnecessary in tokenised markets. That opportunity is rich in testing challenges, such as instant cross-border payments and intra-day interest, and they cannot be met without investment in new systems and infrastructures.

Not just funds but traditional and tokenised asset markets as a whole are converging on a single model already. That convergence must culminate in integration. The trading of digital assets is increasingly indistinguishable from the trading of conventional assets. Even regulators are designing rules to ensure that tokenised assets are regulated in the same way as traditional assets. TradFi and DeFi are becoming one.