What cryptocurrency services institutional clients want

- 21 hours ago

- 4 min read

Institutional asset and wealth managers and end-investors are increasingly active in the cryptocurrency markets. This is putting the banks that provide them with trade and post-trade services in the traditional markets under pressure to make it easy for buy-side institutions to access cryptocurrency markets, trade cryptocurrencies, settle cryptocurrency transactions and safekeep and service cryptocurrency assets in custody. In a webinar sponsored by Börse Stuttgart Digital, experts from BBVA, Deka Bank, Swissquote and Börse Stuttgart Digital discussed whether banks should build client-facing cryptocurrency services in-house, buy a platform from a vendor or outsource the service to an established provider.

Traditional banks are offering cryptocurrency services to institutional clients partly for commercial reasons (cryptocurrency trading is a high margin business), partly for strategic reasons (cryptocurrencies fit within broader digital asset ambitions) but mainly for defensive purposes (to prevent clients defecting to third parties which might offer them conventional asset services as well).

Chart 1

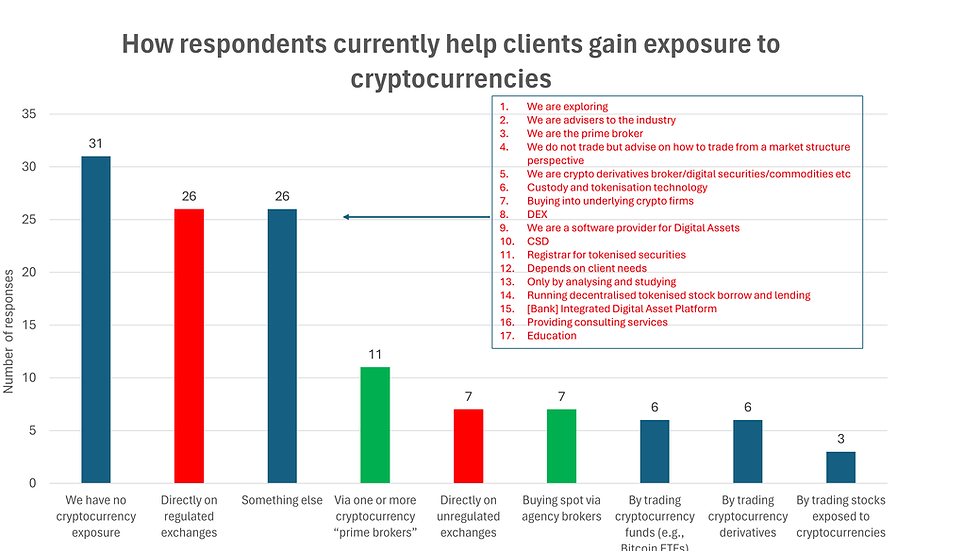

80 per cent of the webinar audience active in cryptocurrency markets already (on their own account or on behalf of clients or both) were aiming their services at institutional clients (see Chart 1). A third accessed the markets for clients via regulated or unregulated exchanges, a fifth via agency or prime brokers and a sixth via proxies such as funds, derivatives and stocks exposed to cryptocurrencies, including corporate treasuries (see Chart 2).

Chart 2

Regulatory changes (such as MiCAR and the GENIUS Act) have lowered the barrier to institutional participation in cryptocurrency markets, but banks have faced technical challenges in giving clients access to the markets. They have had to decide if the technical obstacles were best cleared by building services in-house, buying a platform from a vendor or outsourcing the service to an established provider.

Banks recognise it is essential to own the client interface, to minimise the risk of losing clients to third parties. For some banks, that translated into retaining control by providing a cryptocurrency custody service first and leaving trading and staking services to later. For other banks, it meant getting a service in place quickly, using third party custodians and brokers, almost irrespective of the associated loss of control and counterparty risk.

Banks that launch their cryptocurrency services with a custody offering only, eschewing trading and staking services, are addressing a palpable client priority. For the audience, asset safety was the top post-trade priority, followed by settlement (see Chart 3). In an asset class prone to hacks and lost private keys, institutions value assurance that assets will be kept and exchanged safely, and that they will be made whole if assets go missing.

Chart 3

Yet banks that lead their cryptocurrency offering with custody, eschewing the risks associated with trading and staking, also take a less visible risk. Offering a pure custody service does not relieve banks of the obligation to screen the source of assets coming into custody. It can also make it more difficult to screen effectively, since they must rely on indirect assurances from end-clients and intermediaries.

On the other hand, banks that emphasise speed to market are usually looking to capture revenues immediately, protect their client base, limit up-front investment costs and avoid inadvertent compliance breaches. Interestingly, once a service is up and running, they rarely retain the combination of third-party services and technologies they chose initially. Indeed, they look to bring as many services in-house as soon as possible.

So, it is not surprising that, of audience members offering cryptocurrency services, half built their platform in-house (see Chart 4). A further quarter use some combination of in-house and vendor technologies plus a third-party service provider. Only a fifth rely on digital asset platforms offered by a custodian, integrated with traditional services from the same provider, and just 5 per cent bought a cryptocurrency platform from a technology vendor.

Chart 4

As regulated financial institutions, banks are constrained in the range of suppliers they can work with. Any service partner must not imperil compliance with the capital, governance, operational resilience, financial crime and best execution obligations laid on banks. Once these standards are met, and integration and connectivity are settled, vendors and service providers struggle to differentiate their offerings.

Banks limit the cryptocurrencies they support. Though some extend their range in adventurous jurisdictions, clients that trade down the quality curve must find other routes to market, such as accessing exchanges directly. Banks look to grow horizontally rather than vertically, positioning cryptocurrencies within a grander strategy that anticipates large-scale tokenisation of money, securities, funds and physical assets.

Long-term extension into other tokenised asset classes is not unimportant for the clients of the banks – they want future-proofed services (see Chart 5) – but the audience emphasised four more urgent priorities. These were liquidity (the ability to buy and sell readily), price quality (trading without moving prices), access to as many sources of liquidity as possible, and cheap and easy switching between on-chain and off-chain cash (see Chart 5 again).

Chart 5

In theory, every outsourced provider aims to deliver on all four priorities. In practice, regulated providers servicing regulated clients can interact with regulated counterparties only. This precludes important sources of liquidity such as automated market-makers. In cryptocurrency markets that are fragmented, automated and open 24/7, customer loyalty is also absent. The briefest service interruption moves orders elsewhere.

Chart 6

But it is a mistake to over-emphasise the importance of trading issues in cryptocurrency services purchasing decisions. The audience attached importance to asset safety (see Chart 6) and especially compliance, in a field where laws and regulations are still developing, and financial crime and data privacy rules are enforced robustly (see Charts 7 and 8). Post-trade services and compliance are at least as important to buyers as efficient trading.

Chart 7

Chart 8

Institutional money active in cryptocurrency markets is demonstrably demanding. The audience were clear that they seek comprehensive services, available on a modular basis, that are priced competitively and offer efficient trade execution through access to multiple sources of liquidity despite the fragmentation of the marketplace, without compromising on the safety of assets in custody or compliance with laws and regulations (see Chart 9).

Chart 9

It would be surprising if client demands do not lead to consolidation of service provision in the cryptocurrency markets. This is happening already. The consolidation is proceeding chiefly at the national rather than the regional level, in line with the commoditisation of services, which increases the value of branding and networks at the country level; the growing burden of regulatory compliance; and the need for scale.